The Splendor and Misery of Modern Banking

Bank collapses and bailouts are part and parcel of how the system "works"

In the last month we have witnessed the second- and third-largest bank failures in the history of the United States. Silicon Valley Bank (SVB) was placed under the receivership of Federal Deposit Insurance Corporation on March 10, 2023. Two days later Signature Bank bit the dust, being closed by regulators from the New York State Department of Financial Services. A third bank, Silvergate, had released a public notice of its intention to submit to a voluntary liquidation on March 8, and several more regional banks (First Republic and PacWest specifically) would begin teetering at the edge of solvency a week or two later.

These bank failures have led to concerns that the banking system might be on the verge of a system-wide collapse. Such fears are often accompanied, somewhat incongruously, by indignation over “bailouts.” While these banks are not in point of fact being rescued, the federal government, through the auspices of the FDIC, did perform a “bailout” of all of SVB’s depositors, including those who held assets beyond the federal imposed insurability limit of $250,000. That our ruling elites would go to such lengths testifies to very real fears within official quarters of a system-wide collapse.

This policy of insuring banking deposits without limit has drawn heavy criticism, especially among so-called populists and other anti-establishment types, who regard such policies as tantamount to socialism for the rich. That is of course true to some extent—although at the same time, it must be admitted that there is more to this than just an effort to shield wealthy people from the hazards of the market. Not everyone with banking accounts with more than $250,000 is a member of the idle rich or the ruling class. Some of these depositors are small businesses scrambling to meet their payroll obligations. Or they may be struggling business trying to amass liquidity to pay off heavy debts. Whatever may in fact be going on at the ground level, the prospect of thousands of depositors no longer having the money to pay off their obligations is fraught with systemic risks. If Peter loses all his savings deposits above $250,000, it’s not necessarily just Peter who must eat this loss. If he had planned to use the bulk of those savings deposits to pay off loans, then his loss will inevitably be transferred to his creditors, who then might not be able to pay off their creditors. Thus a banking failure in one sector of the economy can trigger a string of banking failures in others, until the whole system comes crashing down like the house of cards it too closely resembles. Indeed, these recent banking failures may in some respects have been initially triggered by the bankruptcy-fiasco of FTX, the crypto hedge fund company that went belly up just after the 2022 Congressional elections. Our financial system might very well be in a perilous state, and huge infusions of liquidity (i.e., “bailouts”) from the federal government may be required to prevent a catastrophic system-wide collapse

How did we get in this mess in the first place? Much of the problems stem from the federal government's inordinate deficit spending combined with fractional reserve banking system and a fiat currency untethered to anything of real value such as gold. Such a system requires delicate management on the part of the financial elite. The institution tasked with managing this unwieldy financial arrangement in the United States i, the Federal Reserve. The Red employs three major tools by which it uses to manipulate the supply of money:

The Fed can lower short-term interest rates (which lowers the cost of borrowing for commercial banks, which in turn makes loans less expensive and credit cheaper and more plentiful).

The Fed can reduce the reserve requirement (which means banks can loan out a greater percentage of their total reserves).

The Fed can expand “open market operations” (which means the Fed buys securities held by banks, thereby providing said banks with more cash that can then be loaned out).

Notice how three tools work: they increase the amount of money in circulation by making it easier for the banking system to make loans. Thus the Fed’s main tools for enlarging the money supply involve increasing the amount of credit within the system. Yet that’s not the least of it. When a bank makes a loan, that money will of course be used for various purchases (capital goods, houses, cars, medical bills, etc.). Eventually, this loaned-out money will find its way back into the banking system, where a large portion of these returned funds can be loaned out once again, thus expanding the total amount of credit in the economy and, ipso facto, the money supply as well. Through repeated iterations, the banking system, by essentially recycling the money they’ve lent out, can expand the money supply many times over. The monetary tools utilized by the Fed help facilitate this process. In the 1990s, the Fed’s “easy money” policies helped engineer a massive credit bubble that eventually precipitated the 2008 financial crisis.

Any expansion of credit must bring about a corresponding expansion of debt, since debt is merely credit from the other side of the ledger. A massive infusion of credit into the economy is equivalent to massive increase in total debt. The more frugal and conscientious among us will understand the problem with expanding debt to unheard of levels. In the first place, there’s a limit to how far the debt can be expanded. Businesses and consumers can only take on so much debt. When they have reached their limit, the credit expansion must come to an end. In addition to this, not all debts get repaid. Just as the banking system begins to reach the point where increasing credit becomes infeasible, debt defaults begin to rise and bring upon the inevitable crisis. Just as an increase in credit expands the money supply, a debt default has the opposite effect: it leads to contraction in the amount of money in circulation. Hence the so-called “liquidity trap” which normally occurs in a major financial crisis. With so much bad debt in the system, there’s a panic which causes market participants to try to sell off their assets and put what’s left of their money in something that is deemed “safe,” like gold or tangible property.

It’s at this point that the federal authorities have to step in and “reliquify” the system through “bailouts” and the like. Of course, such bailouts are very unpopular among the subject class. But there doesn’t seem to be any help for them. If the financial system were allowed to just collapse the economic devastation would be far worse. As long as we have this system of credit expansion combined with fiat money, periodic “bailouts” of the financial institutions regarded as “too big to fail” is par for the course. There’s no way around it.

Would a return to the gold standard solve this problem? It would, but only partially. Under a gold standard, we would still see periodic expansions of credit leading to sharp and painful busts, but gold would impose a kind of discipline on financial institutions that would prevent things from getting too far out of hand. With gold there the inevitable day of reckoning tends to come much earlier, because unlike fiat money, gold can’t be created out of thin air. Under the gold standard economic crises would be sharp and painful, but the economy would recover in fairly short order.

The real problem with a gold standard is that it is currently unimplementable. When Richard Nixon took the dollar of the good standard in August of 1971, he didn’t do so out of some kind of premeditated villainy. He really had no choice. The Vietnam War and the Great Society led to such huge increases in the federal deficit that the U.S. government could no longer meet its financial obligations with a currency backed by gold. A fiat money hence became a necessary evil.

Conspiracy theorists have in recent years raised concerns that our current fiat “paper” currency will be replaced by a “digital” currency, thus enabling sinister forces within the ruling class to monitor, and potentially control, everything we do with our money. Undoubtedly, there are powerful individuals within the ruling elite who would only be too thrilled to have such an arrangement. But implementing such a thing would pose huge challenges. There are still pockets within the economy where cash is king; and if the dollar-based currency were removed, those who prefer cash would be forced to make use of some kind of substitute—gold and silver coins, for example, or perhaps foreign currencies such as the Euro and even the Yuan. What is more likely is that a digital dollar will be introduced as an adjunct of sorts to the paper dollar. Indeed, in some respects this has already happened. Credit cards are almost like a digital currency, since the money they stand for is little more than digits stored on some computer’s hard-drive.

Even if a transfer to an all-digital currency ends up taking place, this won’t fundamentally change the dynamics of credit expansion facilitated by fiat money. So for the immediate future, we are pretty much stuck with the system we have. Now some may be wondering: if such a system is so fraught with peril, leading, as it most inevitably does, to these massive debt defaults that put the entire system at risk, wouldn’t even the elites themselves want to devise a system with less inherent risk? The answer to this question is an emphatic no. The financial elites derive great benefits from the current system, and despite its obvious shortcomings, it does feature several advantages that could be put forth in its favor. Perhaps the chief benefit of this system is that, by making credit greatly more plentiful, it creates opportunities for entrepreneurs that might not exist under a more strict, if more stable, arrangement.

Let us imagine, for argument’s sake, a financial system that somehow or other managed to eliminate both fiat money and fractional reserve banking. Under such a system, banks could only lend out what they held in savings and checking deposits—not a dollar more. In other words, they could not loan out money that had already been loaned out (regardless by whom). This would prevent banks from having the ability to increase the size of the money supply by recycling loaned funds. Such a system would likely be remarkably stable and “safe.” But it would not necessarily create the most ideal conditions for fostering the sort of economic development that transformed the civilized world many times over in the last two hundred years. The problem with confining credit to the amount that is saved is that it is not clear how under such an arrangement risk-taking entrepreneurs will be able to get their hands on enough lucre to fund their innovations. Economic development occurs when entrepreneurs are able to introduce new and untested innovations into the economy. The problem with untested innovations is that they are inherently risky. Now people who save tend to be risk averse. That is, indeed, one of the prime motivations of saving—to create a hedge against uncertainty (i.e., save for the proverbial rainy day). Now if the primary source of credit available in the economy comes largely from risk averse savers, this is going to lead to a mis-alignment of incentives. Risk averse individuals will not want their savings to be invested in business ventures that involve untested (and therefore highly risky) innovations.

Credit inflation has the advantage of breaking down these mis-aligned incentives and making it easier for entrepreneurs to get the money they need to fund their untested schemes. When an economy is awash with credit, it creates an illusion of prosperity and plentiful capital that (1) renders market participants, including risk averse saves and bank loan managers, more optimistic and hence more willing to lend their savings to innovative entrepreneurs, and (2) creates a large fund of money to draw from for lending purposes. Of course, if credit expansion via fractional reserve banking and fiat money make it easier for entrepreneurs to raise the capital necessary to introduce their game-changing innovations in the economy, it also for very similar reasons makes it easier for bad entrepreneurs (and speculators and outright frauds) to get their grubby hands on credit as well. Money lent to bad entrepreneurs and other such frauds will likely never get paid back. Hence from the start a credit expansion, even if it is managing to get money into the hands of economic innovators, is at the same time sowing the seeds for the inevitable day of reckoning.

If the money created through credit expansion is mainly loaned out for the purposes of buying capital goods, this will cause the prices of capital goods to surge, which will put a strain on businesses that need to purchase capital goods and now have to pay more than they initially budgeted. But these cost overruns won’t necessarily harm businesses introducing new innovations into the economy, because these new innovations will in a sense pay for themselves. An economic innovation introduces efficiencies of some sort or another into the economy. Either it decreases the costs of production or introduces a new kind of product that more efficiently satisfies the needs of consumers. Either way, economic productivity is increased and the economy produces more with less. The efficiencies introduced by innovations can thus make up for any increases in cost of capital goods due to credit expansion. But it is only the business introducing these innovations that will benefit from these efficiencies. Businesses that are not innovating, that are either following tried and true practices or have introduced bad innovations (i.e., innovations that decrease economic productivity)—such businesses must shoulder the greater costs of capital goods during credit expansion, and if those businesses are paying for their capital expenditures through loans, they may struggle to repay these debts. This will inevitably lead to a rise in credit defaults and bankruptcies, which will in turn usher in a debt crisis that will bring about a great contraction of economic activity—that is, a recession or, if it’s really bad, a depression. Once all the bad debt (along with the bad businesses associated with that debt) are cleared from the system, the whole process can begin anew with a fresh wave of credit expansion.

To be sure, this is but a very rough sketch of how the entire process evolves over time. In the real economy, matters are greatly more complicated. Nor can we always assume that the mis-alighnment of incentives between savers and risk-taking entrepreneurs will always be as stark as I have presented it. The broader point to keep in mind is that whatever disadvantages may arise from a system of unbridled credit expansion, we cannot accuse it of being incompatible with economic growth and prosperity. Although we’ve had credit expansion through fractional reserve banking at least since the Renaissance, and fiat money since 1971, this has done little to hinder, and may have even helped foster, a series of tremendous economic innovations that has utterly transformed the lives of those living in the nations of the civilized world. The only question is whether we can expect this entire process to work nearly as well in the future as it has in the past; for there are some indications that the system may be evolving into a more dysfunctional state, one which may not be fully compatible with growth rates we have seen historically.

A system of credit expansion (via fractional reserve banking and fiat money) can “work” after a fashion if enough of the money generated by credit expansion can find its way into the hands of entrepreneurs capable of using those funds for introducing revolutionary innovations into the economy. If this process is in some serious way compromised, either because (1) the excess credit for some reason or another does not find its way into the hands of innovative entrepreneurs, or because (2) no such “innovative” entrepreneurs exist any longer; then, in either case, all the funds generated by credit expansion will go to waste and the economy will merely be spinning its wheels to no purpose.

One sure sign that something along these lines might be happening is when we find an increasing share of money generated by credit expansion flowing, not into innovative businesses, but into over-inflated assets. Since the 1980s, more and more of the economy’s total investment has been siphoned into stocks, bonds, crypto, derivatives, and the like, thus pushing the price of these assets well beyond their intrinsic worth. This opens up a wide field in which a handful speculators can rake in huge amounts of money without, however, doing much in terms of moving the economy forward. Over time, stock exchanges and asset markets begin to take on the appearance and function of rigged gambling establishments rather than as vehicles for efficient capital allocation. Huge fortunes are made by taking shrewd advantage of fluctuations in the prices of stocks, bonds, and derivatives rather than investing in game-changing innovations. When too much of the wealth of financial elites is derived from speculation fostered by credit expansion, that means that the system has become so unwieldy and dysfunctional that it is not clear how much longer it can go on.

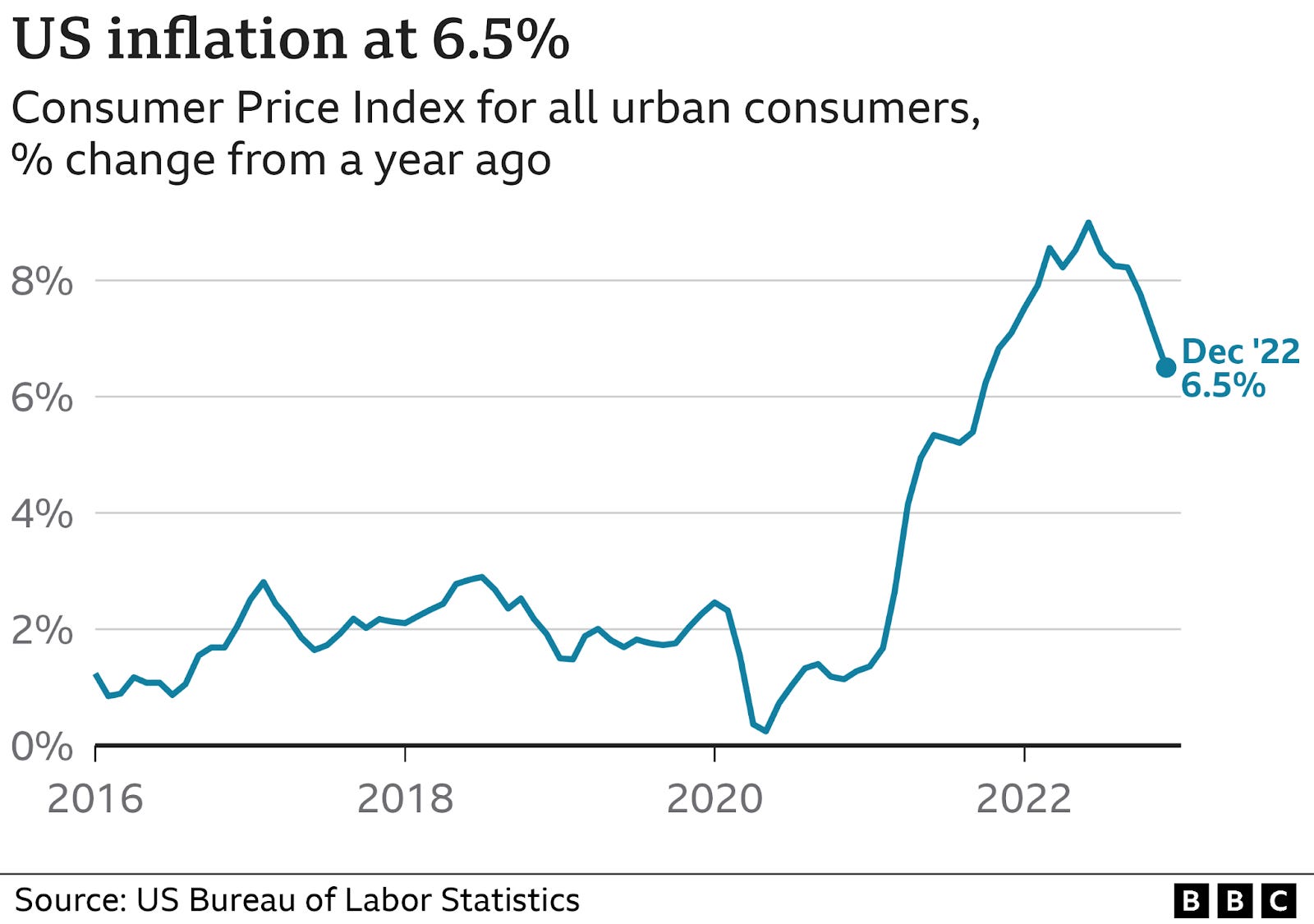

For the last few decades the inflationary excesses of the system have been confined primarily to assets and housing. But because of the grievous effects of the Covid-19 lockdowns on supply chains, this inflation has begun to spill out into the economy at large. The following chart illustrates the surge in price inflation in the wake of those disastrous lockdowns:

These rising prices have put the squeeze on the nation’s financial system, which is reeling as a consequence. Hence the desperation of financial elites to bailout the depositors of Silicon Valley Bank. It may be wondered, however, if banks continue to collapse, where will the federal government get the money to bailout all any depositors who end up losing all or most of their savings? If the banking system goes belly-up, how will the Federal Reserve, as the lender of last resort, reliquify the system? As in 2008, the Fed will have no choice but to create money “out of thin air” to replace the money that had disappeared as a consequence of debt defaults. But wouldn’t such a procedure (essentially the digital equivalent of “printing money”) lead to even greater inflation? Actually no, it would not make inflation worse. This may seem counter-intuitive, but it’s nonetheless true. As I noted earlier, under a banking system that combines fiat money with fractional reserve banking, any money lost to bankruptcies leads to a contraction in the money supply; for just as credit expansion increases the amount of money in circulation, so debt cancellation inevitably leads to a contraction in the money supply—that is to say, a deflation. This is precisely what occurred, for example, in 2008, as the following chart illustrates:

Note that during the worst months of the crisis, the inflation rate was negative. This happened despite the frantic efforts by the Bush administration and the Fed to reliquify (i.e., bailout) Wall Street and the banks.

However unappetizing the bailouts of 2008 may have been, they were necessary to prevent an even more catastrophic system-wide collapse. The real tragedy of 2008 was not the bailout;, it was the fact that no efforts were made to reform the system. To be sure, true reform would have been extremely difficult, if not impossible; for it would involve (1) ending once and for all the policy of chronic deficit spending on the part of the Federal government and (2) reattaching the dollar to gold. Only with a return to fiscal responsibility and the gold standard can the system of credit expansion followed by endless “bailouts” through reliquification be ended once and for all.

Greg Nyquist is author of The Psychopathology of the Radical Left and The Faux-Rationality of Ayn Rand.